The World Gold Council’s ‘Gold Demand Trends Q1 2024 report presents a complex landscape for gold demand.

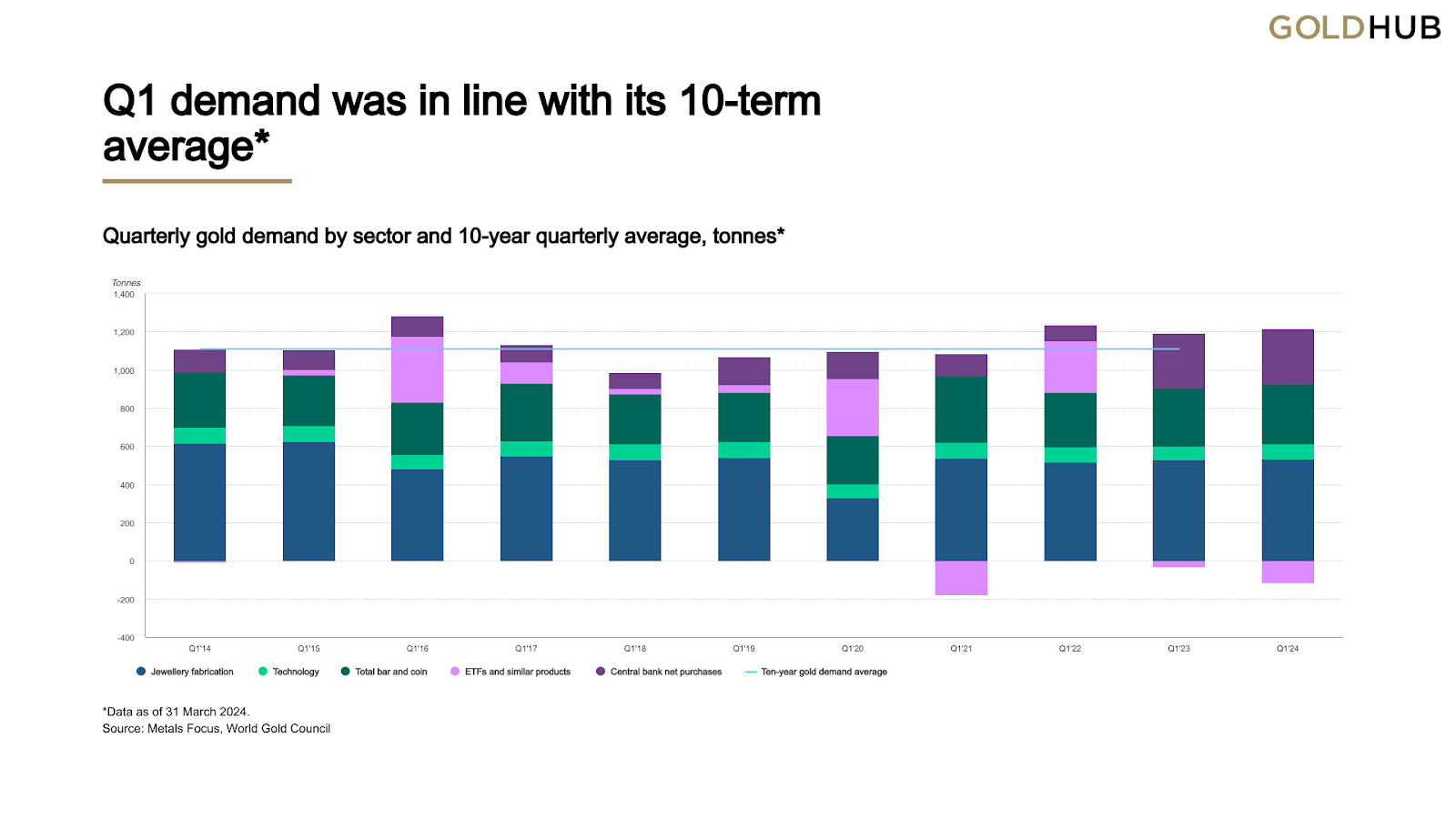

When including over-the-counter (OTC) transactions, total demand saw a year-on-year increase of 3% to 1,238 tonnes, bolstered by significant purchases by central banks and OTC investments. This was against a backdrop of a 5% drop in demand excluding OTC transactions, which fell to 1,102 tonnes due to continued outflows from exchange-traded funds (ETFs).

Central Bank and OTC Influences

Central banks significantly increased their gold holdings, with a net addition of 290 tonnes, although not all additions are currently shown in International Monetary Fund (IMF) data. Investor buying in the OTC market significantly impacted gold prices during the quarter. The average price reached $2,070 per ounce, marking a 10% increase from the previous year and a 5% increase from the previous quarter, with prices peaking at $2,214 per ounce by the end of March.

Sector-Specific Demand

- Jewelry: The jewelry sector showed a slight decrease in consumption by 2% to 479 tonnes. Jewelry fabrication increased by 1% year-on-year to 535 tonnes, leading to an inventory build-up of 56 tonnes.

- Bar and Coin: Demand remained consistent at 312 tonnes, showing a 3% increase year-on-year.

- ETFs and Investment Products: There was a net decrease in gold ETF holdings by 114 tonnes, primarily due to reductions in Europe and North America, though this was somewhat offset by gains in Asia. Notably, U.S.-listed funds showed positive movements towards the end of the quarter.

- Technology: Demand for gold in technological applications, particularly in electronics driven by the AI boom, increased by 10% year-on-year.

Production and Recycling

Gold mining production saw a 4% year-on-year increase, reaching a record 893 tonnes for the first quarter. Gold recycling also increased by 12% year-on-year, achieving 351 tonnes, the highest quarterly figure since the third quarter of 2020.

Regional Investment Differences

Investor behaviour varied between Western and Eastern markets. Western investors continued strong purchasing but also took profits. In contrast, Eastern markets saw strong buying amid rising prices, indicating a regional difference in investment approaches.

Implications for the Jewelry Industry

For jewellers, the current gold market presents both challenges and opportunities. The slight decrease in global jewelry consumption could lead to reevaluating inventory levels and cost management strategies, especially considering the recent inventory increase. The rise in gold recycling provides an alternative source of materials, which could influence pricing and supply strategies.

With record gold prices and diverse investment behaviour, jewellers will need to remain flexible and strategically aware to effectively navigate the evolving market conditions.