In an unprecedented shift within the diamond industry, Russia has surpassed Botswana as the leader in rough-diamond production value for the first time in 2023.

Despite facing stringent sanctions and a challenging market, Russia’s rough-diamond production achieved a significant milestone, according to the latest Kimberley Process (KP) statistics released this week.

Key Production Figures

Russia produced 37.3 million carats of rough diamonds in 2023, valued at $3.61 billion. This represents an average price of $97 per carat, marking a notable increase from the previous year’s output of 41.9 million carats, valued at $3.55 billion with an average price of $85 per carat.

This rise in value is significant given the geopolitical and economic challenges the country faces, including expanded sanctions from the European Union and stricter regulations from the United States on goods processed in third-party countries such as India.

Conversely, Botswana’s diamond production value saw a decline. The country produced 25.1 million carats in 2023, valued at $3.28 billion, with an average price of $131 per carat. This is a decrease from 2022 when Botswana’s output was 24.5 million carats, valued at $4.7 billion, with an average price of $192 per carat. The reduction in value is partly attributed to a lower output mix from De Beers’ Jwaneng mine, which is currently undergoing expansion.

Global Production Trends

Globally, rough-diamond output fell by 20% year on year to $12.72 billion. By volume, production decreased by 8% to 111.5 million carats. Total imports dropped by 10% in volume, and global exports declined by 9%. This downturn reflects significant decreases in the number of carats exported from major producing countries: a 12% drop from Russia, a 24% reduction from Botswana, and a substantial 45% decrease from South Africa.

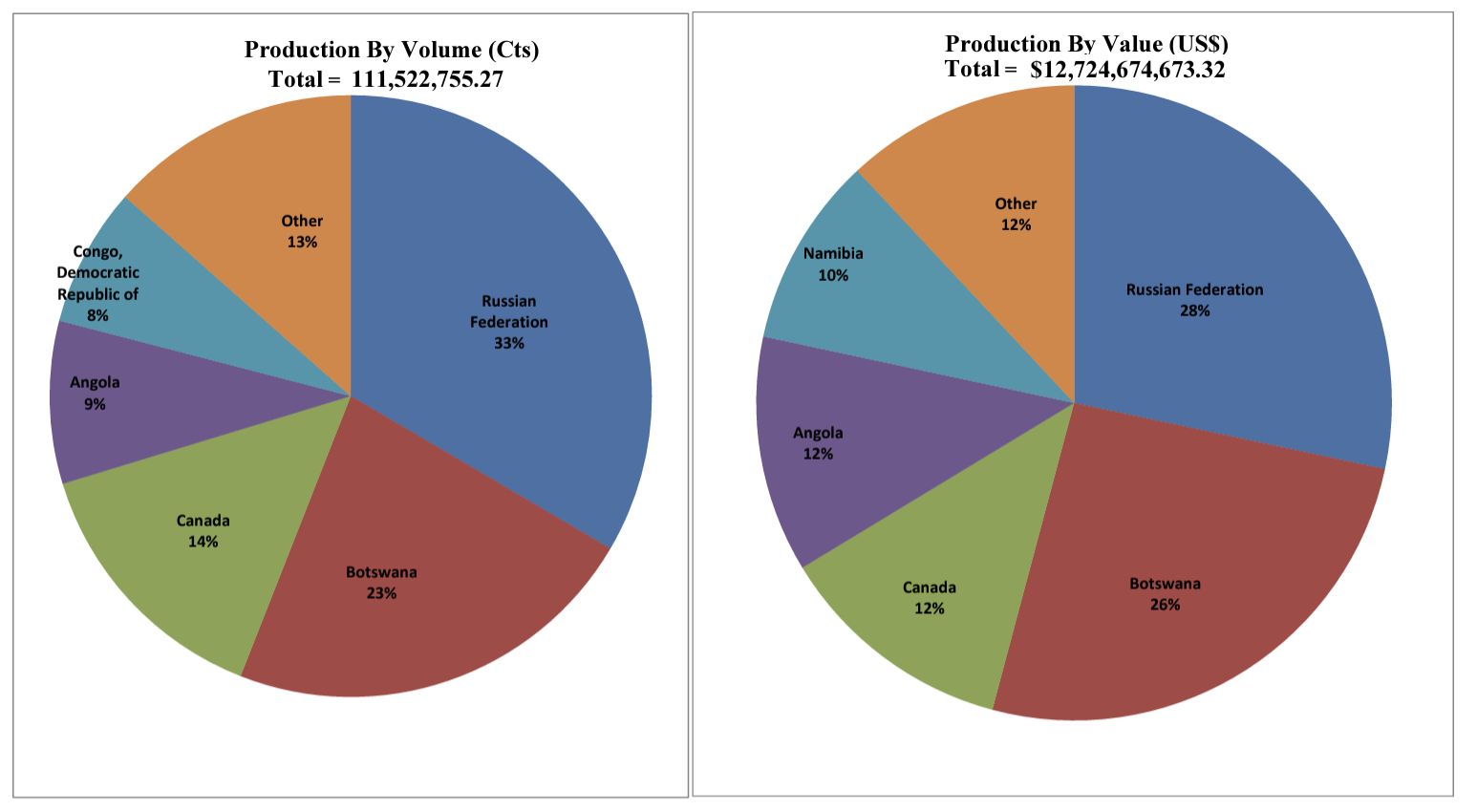

Production by Volume and Value

The accompanying graphs highlight the distribution of diamond production by volume and value across different countries in 2023.

Production by Volume (Cts):

- Russian Federation: 33%

- Botswana: 23%

- Canada: 14%

- Angola: 9%

- Congo, Democratic Republic of: 8%

- Other: 13%

Production by Value (US$):

- Russian Federation: 28%

- Botswana: 26%

- Canada: 12%

- Angola: 12%

- Namibia: 10%

- Other: 12%

Industry Implications

For jewellers and industry stakeholders, the shifting landscape of diamond production underscores the importance of monitoring geopolitical developments and their impact on the supply chain. The rise of Russia in production value, despite facing international sanctions, suggests resilience and potential strategies that could influence market dynamics. The decrease in Botswana’s output value, amid expansion efforts at major mines, highlights the volatility and risks associated with production scalability and market demands.